Over the decades, perhaps you’ve been very good at saving your money and investing it for long-term growth. But when the time comes for you to stop working or to step back to a part-time job, you might need to shift your focus. It is time to think about income.

When you were decades away from retirement, you may have leaned toward a portfolio that was mainly invested in the stock market. This was a good strategy: According to FactSet, the benchmark S&P 500

SPX,

has had an average annual return of 9.88% over the past 30 years, with dividends reinvested. Nearly 80% of stocks in the S&P 500 pay dividends, and reinvestment is a core element of the compounding that has made stocks such a reliable vehicle for long-term growth.

Investing in the S&P 500 is simple, too, by purchasing shares of the SPDR S&P 500 ETF Trust

SPY,

or other index funds that track the benchmark. There are many similar funds, and plenty of them have very low expenses.

Of course, a long-term growth investor whose portfolio is mainly invested in the stock market needs to resist the temptation to sell into declining markets. Attempts to time the market tend to lead to underperformance when compared with the S&P 500, because investors who move to the sidelines tend to return too late after a broad decline has been reversed.

And brutal declines in the stock market are typical. It’s not uncommon for the market to fall by 20% or even more. But through it all, that 30-year average return has remained close to 9.9% — and if you look even further back, that average return has been nearly the same.

Your life has changed, and you need income

Now imagine that you’re 60 years old and you need to stop working, or perhaps you just want to work part time. After decades of saving and investing for growth, how do you prepare for this change?

It is important to take an individual approach to your income needs, says Lewis Altfest, CEO of Altfest Personal Wealth Management, which oversees about $1.6 billion in assets for private clients in New York.

Think about what type of accounts you have. If your money is in a 401(k), IRA or another tax-deferred account, everything you withdraw will be subject to income taxes. If you have a Roth account, for which contributions were made after tax, withdrawals from that account won’t be taxed. (You can read about conversions to Roth accounts here.)

If you have a tax-deferred retirement account that is sufficiently large and you want to continue pursuing long-term growth with stocks (or funds that hold stocks), you might consider what’s known as the 4% rule, which means that you’ll withdraw no more than 4% of your balance a year — as long as that is enough to cover your income needs. You might begin by simply setting up an automatic withdrawal plan to provide this income. Of course, to limit your tax bill, you should withdraw only as much as you need.

The 4% rule

That 4% rule is a useful starting point for conversations with clients who need to begin drawing income from their investment portfolios, says Ashley Madden, the director of financial planning services at Hutchinson Family Offices in Greensboro, N.C., but it shouldn’t be a hard-and-fast rule. “Like most financial-planning concepts, I don’t think the 4% safe-withdrawal rate is ‘one size fits all’ for all planning situations,” she says.

Rather, you should think about how much you’ll need to withdraw to cover your expenses, including healthcare, while still allowing your investment account to grow, Madden says. Consider all your income sources, your anticipated expenses, the types of investments in your portfolio and even your estate planning.

Madden has worked with clients who have taken much more than 4% from their investment accounts during their early retirement years, which she says concerns her as an adviser. She says this is when a discussion of the 4% withdrawal concept can help “illustrate how they are taking money out at a more rapid rate than the investments can grow.”

The idea of a 4% withdrawal rate can also help during discussions with retirees who are reluctant to withdraw any income at all from their investment accounts, Madden says.

In either scenario, thinking about withdrawals as a percentage, rather than a dollar amount, can help “to empower decision-making by removing some emotion from the process,” she says.

Generating income

When it comes to generating income, here are a few approaches to consider:

- Investing in bonds, which make regular interest payments until they mature. You might also pursue bond income through funds, which have diversified portfolios that can lower your risk.

- Taking dividend income from stocks you hold, rather than reinvesting those dividends.

- Purchasing some individual stocks with attractive dividend yields to receive income while also aiming for some growth as the share prices rise over the long term.

- Selecting a few mutual funds or exchange-traded funds that hold stocks for dividend income. Some of these funds might be designed to augment income while lowering risk with covered-call strategies, as described below.

As you think about planning for retirement and about making changes to your investment strategy as your objectives evolve, consider meeting with a financial planner as well as an investment adviser.

Bonds and the 60/40 allocation

You may have read articles discussing what’s known as the 60/40 portfolio, which is one made up of 60% stocks and 40% bonds. MarketWatch contributor Mark Hulbert has explained the long-term viability of this approach.

The 60/40 portfolio is “a good starting point for discussions with clients” about income portfolios, says Ken Roberts, an investment adviser with Four Star Wealth Management in Reno, Nev.

“It is an approximation,” he notes. “If one asset class is growing, we might let it go. If there is an opportunity in another class, we might take advantage of it at the right time.”

In a January report titled “Caution: Heavy Fog,” Sharmin Mossavar-Rhamani and Brett Nelson of the Goldman Sachs Investment Strategy Group wrote that the 60/40 portfolio is “used generically by the financial industry to mean a portfolio of stocks and bonds; it does not imply that a 60/40 mix is the right allocation for each client.”

Both Roberts and Altfest point to opportunities in the bond market right now, in light of the increases in interest rates that have pushed bond prices down over the past year. Altfest suggests that in this market, a portfolio of two-thirds bonds and one-third stocks would be appropriate for an income-oriented portfolio, because bond prices have declined as interest rates have soared over the past year.

Altfest notes that for most investors, taxable bonds feature more attractive yields than municipal bonds.

If you buy a bond, your yield is the bond’s annual interest payments (the coupon, or stated interest rate, divided by the face value) divided by the price you pay. And if you buy at a discount to the bond’s face value and hold the bond until maturity, you will realize a capital gain. If interest rates rise after you buy a bond, you are sitting on an unrealized gain, and vice versa.

“Bonds give you a yield now, and if we go into a recession, you become a winner as opposed to a loser with stocks,” Altfest says. In other words, during a recession, the Federal Reserve would likely lower interest rates to spur economic growth. That would push bond prices higher, giving you the potential for “double-digit annual returns,” according to Alftest.

We cannot predict which way interest rates will go, but we know that the Fed’s policy of lifting interest rates to push down inflation cannot go on forever. And when you factor in the current price discounts, relatively high yields and eventual maturity at face value, bonds are compelling right now.

It can be difficult to build a diversified bond portfolio on your own, but bond funds can do the work for you. A bond fund has a fluctuating share price, which means that when interest rates rise, there is downward pressure on the share price. But at the moment, most of the bond-fund portfolios are made up of securities trading at discounts to their face values. This provides downside protection along with the potential for gains when interest rates eventually begin to decline.

Altfest recommends two bond funds that mainly hold mortgage-backed securities.

The Angel Oak Multi-Strategy Income Fund

ANGIX,

has $2.9 billion in assets under management and quotes a 30-day yield of 6.06% for its institutional shares. It is mainly invested in privately issued mortgage-backed securities.

The $33.8 billion DoubleLine Total Return Bond Fund

DBLTX,

has a 30-day yield of 5.03% for its Class I shares and is a more conservative choice, with over 50% invested in mortgage-backed securities and government bonds.

For traditional mutual funds with multiple share classes, institutional or Class I shares, which might be known as adviser shares, typically have the lowest expenses and highest dividend yields. And despite the names of the share classes, they are available to most investors through advisers, and often through brokers for clients who don’t have an adviser.

For investors who aren’t sure what to do immediately, Roberts points to short-term U.S. Treasury funds as a good alternative. Two-year U.S. Treasury notes

TMUBMUSD02Y,

now have a yield of 4.71%. “You might ride out the next couple of years and look for opportunities in the market,” he says. “But averaging in [to longer-term bonds] as the Fed gets closer to its terminal rate, before it pauses and then begins to cut, can work out quite well.”

Then there are municipal bonds. Should you consider this option for tax-exempt income in the current environment?

Altfest says the spread between taxable and tax-exempt yields has widened so much over the past several months that most investors would be better off with taxable bonds. To back that notion, consider the Bloomberg Municipal Bond 5-year index, which has a “yield to worst” of 2.96%, according to FactSet. Yield to worst refers to the annualized yield, factoring in a bond’s current market value, if the bond is held to its maturity date or call date. A bond may have a call date that is earlier than the maturity date. On or after the call date, the issuer can redeem the bond at face value at any time.

You can calculate a taxable equivalent rate by dividing that 2.96% yield by 1, less your highest graduated income-tax rate (leaving state and local income taxes aside for this example). Click here for the Internal Revenue Service’s list of graduated tax rates for 2023.

If we incorporate the graduated federal income-tax rate of 24% for a married couple who earned between $190,750 and $364,200 in 2023, our taxable equivalent for this example is 2.96% divided by 0.76, which comes to a taxable equivalent of 3.89%. You can earn more than that with U.S. Treasury securities of various maturities — and that interest is exempt from state and local income taxes.

If you’re in one of the highest federal brackets and in a state with a high income tax, you might find attractive-enough tax-exempt yields for bonds issued by your state or municipal authorities within it.

An alternative to bonds for income: Dividend yields on preferred stocks have soared. This is how to pick the best ones for your portfolio.

Stocks for income

There are various approaches to earning income from stocks, including exchange-traded funds and individual stocks that pay dividends.

Remember, though, that stock dividends can be cut at any time. One red flag for investors is a very high dividend yield. Investors in the stock market might push a company’s shares lower if they perceive problems — sometimes years before a company’s management team decides to lower its dividend (or even eliminate the payout).

But dividends (and your income) can also grow over time, so consider shares of strong companies that keep raising payouts, even if current yields are low. Here are 14 stocks that doubled in price in five years, even as their dividends doubled.

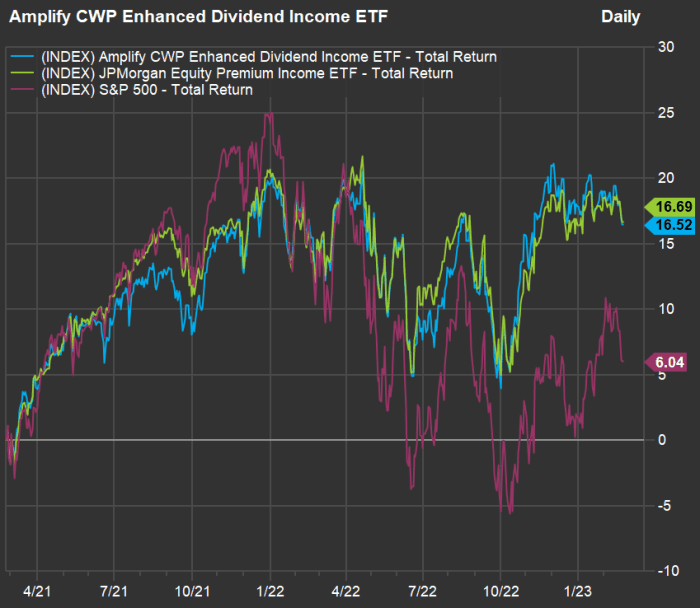

Rather than looking for the highest dividend yields, you might consider a quality-focused approach. For example, the Amplify CWP Enhanced Dividend Income ETF

DIVO,

holds a portfolio of about 25 stocks of companies that have increased dividends consistently and are deemed likely to continue to do so.

This fund also makes use of covered-call options to enhance income and protect from downside risk. Covered-call option income varies and is higher during times of heightened volatility in the stock market, as we have seen over the past year. According to FactSet, this fund’s 12-month distribution yield has been 4.77%.

You can read more about how the covered-call strategy works, including an actual trade example from Roberts, in this article about the JPMorgan Equity Premium Income ETF

JEPI,

which holds about 150 stocks selected for quality (irrespective of dividends) by JPMorgan analysts. According to FactSet, this ETF’s 12-month distribution yield has been 11.35%. In a less volatile market, investors can expect distribution yields in the “high single digits,” according to Hamilton Reiner, who co-manages the fund.

Both of these ETFs pay monthly dividends, which can be an advantage, as most companies that pay dividends on stocks do so quarterly, as do most traditional mutual funds.

Each approach has advantages and disadvantages, and JEPI is less than three years old. Keep in mind that funds that follow covered-call strategies should be expected to outperform the broad index during times of higher volatility and to underperform, at least slightly, during bull markets, when dividends are included.

Here’s a two-year performance comparison of total returns, with dividends reinvested, for the two ETFs and the S&P 500.

FactSet

For the investor who wants to shift a portfolio that is mainly invested in stocks to an income portfolio, Altfest leans heavily toward bonds in this market but says he would still want a client to be about one-third invested in stocks. He would advise a client already holding some individual stocks to sell the more growth-oriented companies and hold onto the ones with decent dividend yields, while also considering how much in profits would be taken when selling stocks that had risen considerably.

“You are more likely to keep those, because you will be saving some money in taxes for the year, than if you sell where you have built a significant nest egg with capital gains,” he says.

And some of those stocks might already be providing significant income relative to the average price the investor has paid for shares over the years.

After making adjustments, you might still want to purchase some stocks for dividends. In that case, Altfest recommends going for companies whose dividend yields aren’t very high, but whose businesses are expected to be strong enough for dividends to increase over time.

To begin, he recommends a screen to narrow down potential stock selections. Here’s what happens if we apply Altfest’s screening parameters to the S&P 500:

- Beta for the past 12 months of 1 or less, when compared with the price movement of the entire index: 301 companies. (Beta is a measurement of price volatility, with a 1 matching the volatility of the index.)

- Dividend yield of at least 3.5%: 69 companies.

- Expected earnings per share for 2025 increasing at least 4% from 2024, based on consensus estimates of analysts polled by FactSet. Altfest suggested going out this far to avoid the distortion of current-year estimates and actual results from one-time accounting items. This brought the list down to 46 companies.

- Expected sales for 2025 increasing at least 4% from 2024, based on consensus estimates of analysts polled by FactSet. The estimates for earnings and sales were based on calendar years, not companies’ fiscal years, which often don’t match the calendar. This last filter narrowed the list to 16 stocks. Alfest then culled the list further, as explained below.

Here are the 16 stocks that passed the screen, by dividend yield:

| Company | Ticker | Industry | Dividend yield | 12-month beta | Expected 2025 EPS increase | Expected 2025 sales increase | |

| Williams Cos. |

WMB, |

Integrated Oil | 5.79% | 0.63 | 7.8% | 10.8% | |

| Walgreens Boots Alliance Inc. |

WBA, |

Drugstore Chains | 5.32% | 0.83 | 11.5% | 4.4% | |

| Philip Morris International Inc. |

PM, |

Tobacco | 5.10% | 0.48 | 10.6% | 7.3% | |

| Iron Mountain Inc. |

IRM, |

Real-Estate Investment Trusts | 4.89% | 0.93 | 9.6% | 9.0% | |

| Hasbro Inc. |

HAS, |

Recreational Products | 4.86% | 0.93 | 21.8% | 8.9% | |

| Kimco Realty Corp. |

KIM, |

Real-Estate Investment Trusts | 4.51% | 1.00 | 6.0% | 10.6% | |

| Truist Financial Corp. |

TFC, |

Regional Banks | 4.42% | 0.97 | 10.7% | 5.0% | |

| Extra Space Storage Inc. |

EXR, |

Real-Estate Investment Trusts | 4.20% | 0.92 | 7.0% | 8.4% | |

| Huntington Bancshares Inc. |

HBAN, |

Major Banks | 4.15% | 0.96 | 9.4% | 5.9% | |

| U.S. Bancorp |

USB, |

Major Banks | 4.04% | 0.79 | 10.0% | 5.4% | |

| Entergy Corp. |

ETR, |

Electric Utilities | 3.98% | 0.53 | 7.4% | 4.6% | |

| AbbVie Inc. |

ABBV, |

Pharmaceuticals | 3.93% | 0.35 | 8.8% | 5.0% | |

| Public Service Enterprise Group Inc. |

PEG, |

Electric Utilities | 3.75% | 0.59 | 10.2% | 6.2% | |

| Avalonbay Communities Inc. |

AVB, |

Real-Estate Investment Trusts | 3.74% | 0.75 | 16.8% | 4.8% | |

| United Parcel Service Inc. Class B |

UPS, |

Air Freight/ Couriers | 3.67% | 0.90 | 12.3% | 6.4% | |

| NiSource Inc. |

NI, |

Gas Distributors | 3.62% | 0.58 | 7.6% | 4.9% | |

| Source: FactSet | |||||||

Click on the ticker for more about each company or exchange-traded fund.

Click here for Tomi Kilgore’s detailed guide to the wealth of information available for free on the MarketWatch quote page.

Remember that any stock screen has its limitations. If a stock passes a screen you approve of, then a different sort of qualitative assessment is in order. How do you feel about a company’s business strategy and its likelihood of remaining competitive over the next decade, at least?

When discussing the results of this stock screen, for example, Altfest says he would eliminate AbbVie from the list because of the threat to earnings and the dividend from increased competition as the patent expires on its Humira anti-inflammatory medication.

He would also remove Philip Morris, he says, because “the movement toward health overseas could bring earnings and dividends down.”